Tax Messenger

The advertising duty: detailed calculation and payment rules proposed

28.03.2025

The provisions of Federal Law No. 479-FZ of 26.12.2024, which introduced a duty on income received for the provision of Internet advertising services (“the advertising duty”), take effect from 1 April 2025. However, the law does not fully address the mechanisms for the calculation and payment of the advertising duty or for monitoring the correct and timely payment of the duty. A detailed summary of the provisions of the law was presented in a previous alert.

On 26 March 2025 the Russian Ministry for Digital Development published a draft decree of the Russian Government “Concerning Approval of Special Considerations Relating to the Calculation and Payment of Mandatory Charges Provided for in Part 1 of Article 18.2 of the Federal Law “Concerning Advertising” and the Procedure for Monitoring the Correct and Timely Payment of Such Charges” (“the Draft Decree”).

The purpose of the Draft Decree is to flesh out the rules for the calculation and payment of the advertising duty and lay down procedures for monitoring the timely payment of the duty by market participants.

The Draft Decree is currently undergoing an anti-corruption review stage (scheduled to end on 1 April 2025) and a public consultation stage (scheduled to end on 15 April 2025). Once the Draft Decree has been approved, its provisions will take effect from its publication date, but not earlier than 1 April 2025.

Overview of key provisions of the Draft Decree

Payers of the advertising duty are advertising distributors, advertising system operators, intermediaries and agents which:

- have concluded an agreement with an advertiser or

- have entered into an agreement with an agent that has an existing agreement with an advertiser or other agents..

The main principle is that there is one payer in the service delivery chain:

- If the advertising duty is paid by one of the participants in the contractual chain that work directly with the advertiser, such as an advertising distributor / an advertising system operator / an intermediary, then the other participants in the contractual chain do not pay.

If the advertising duty is paid by an agent, it pays the duty only on its own agency fee. However, the advertising distributor / advertising system operator / other intermediaries remain liable to pay the duty. In this case, the question remains of how, in a contractual chain in which agents are involved, the duty is to be paid by other participants in the chain that work directly with the advertiser.

However, an agent has the right to pay the advertising duty in full, in which case all the other participants in the contractual chain are exempt from paying the duty.

Thus, the approach to the payment of the advertising duty in relation to each item of distributed advertising depends on the contractual chain and the choice of payer made by the transacting parties.

The base for the calculation of the advertising duty at the rate of 3% is calculated on the following amounts:

- income received by advertising distributors, advertising system operators and intermediaries from Internet advertising services provided under an agreement with an advertiser;

- income of agents that act on behalf of and at the expense of an advertiser and/or an advertising distributor for the performance of an agreement concluded with an advertiser.

Importantly, reported income from the distribution of Internet advertising must be corroborated by account books, service completion certificates and primary documents of the payers of the advertising duty.

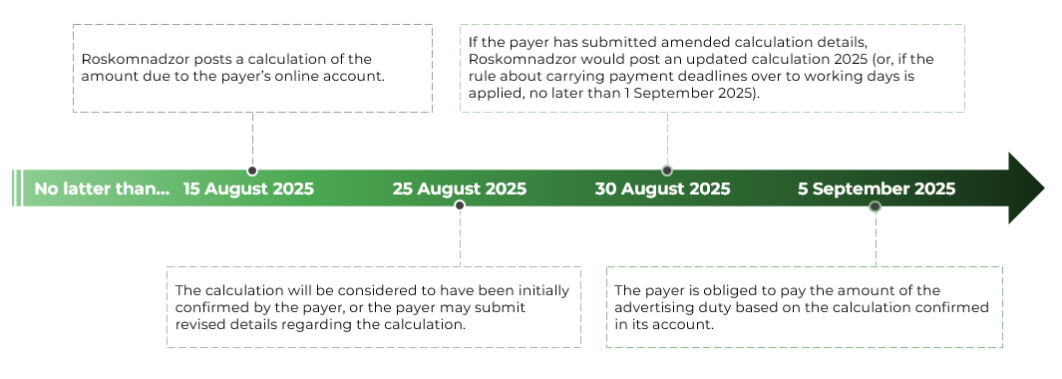

Time limits and procedure for the calculation and payment of the advertising duty

The payment period is each quarter running from the beginning of the calendar year.

No later than the 15th of the second month of the quarter following a payment period, a calculation of the advertising duty payable for the relevant quarter will be generated in the payer’s account on the official website of Roskomnadzor (the Federal Service for Supervision of Communications, Information Technology and Mass Media). That calculation must be checked and confirmed by the payer within 10 calendar days by means of signing it in the account by an enhanced qualified signature or a simple electronic signature.

In addition, the payer has the right to send Roskomnadzor amended calculation details within the same 10 calendar days. Based on the amended details received from the payer, Roskomnadzor would, within 5 calendar days of receiving the amended details, post an updated calculation to the payer’s account. The payer must in turn calculate and confirm that calculation within 10 calendar days of receiving the updated calculation by signing it in the account.

If the payer does not confirm the calculation or submit amended details, the calculation will be automatically considered to have been accepted and confirmed by the payer upon the lapse of 10 calendar days from the date on which it was posted to the account.

The obligation to pay the advertising duty based on the calculation submitted by Roskomnadzor must be fulfilled no later than the 5th of the third month of the quarter following the payment period.

Once Roskomnadzor receives information that payment has been received, it must send a notification of payment to the payer within 1 working day.

Funds paid in excess may be refunded or credited towards future payments through an application to Roskomnadzor.

Thus, taking the second quarter of 2025 as an example, the procedure for the payment of the advertising duty would be as follows:

The procedure for the payment of the advertising duty

Monitoring and verification of the fulfilment of obligations to pay the advertising duty

The timely payment of the advertising duty will be continuously monitored by Roskomnadzor on the basis of information received from duty payers and information on payments obtained from the State Information System for State and Municipal Payments. In this regard, monitoring would be conducted without direct interaction with advertising duty payers.

No later than the 20th of the month preceding the year for which monitoring is to be conducted (i.e., no later than 20 December), Roskomnadzor must submit a monitoring plan to the Russian Ministry for Digital Development. The plan should outline the purpose, timeframes, payer categories, the monitoring deadline, and the procedure for submitting the monitoring results report.

After the end of a monitoring period (i.e., a year) and no later than the 20th of the month preceding the following year (i.e., no later than 20 December), Roskomnadzor must submit to the Russian Ministry for Digital Development a monitoring report containing lists of payers / non-payers of the advertising duty.

If, in the course of monitoring, Roskomnadzor identifies cases of the non-payment / underpayment of the advertising duty, the payer will be notified of the identified violation and its right to provide an explanation for that violation no later than 7 working days from the date of receipt of the notification of the violation. If Roskomnadzor does not accept the payer’s explanation or the payer does not provide one, Roskomnadzor will issue a demand for the payment of advertising duty. If the payer does not settle the advertising duty within 10 calendar days, the amount in question will be collected through court proceedings.

Thus, the process outlined above for monitoring the timely payment of the advertising duty is established to ensure the full payment of amounts due to the Russian state.

Important considerations for businesses in connection with the proposed rules for the payment of the advertising duty

In light of the increased fiscal and administrative burden on advertising business, we recommend taking immediate action to address the following key aspects:

-

Negotiating with counterparties in the service delivery chain for the distribution of Internet advertising to determine the “rules of play”, i.e. to obtain a clear understanding of how the advertising duty should be calculated and paid in relation to each item of Internet advertising that is distributed.

-

Analysing the list of services provided to identify services that are directly related to the distribution of Internet advertising.

-

Analysing the company’s approach to the positioning of its services in public sources.

-

Analysing types of agreements (service agreement vs agency agreement) and related documents to determine the following aspects:

- which services under the agreement are assessable to the advertising duty;

- which participant in the chain is responsible for paying the advertising duty;

- commercial provisions concerning the liability of participants in the chain for the non-fulfilment of obligations to pay the advertising duty and the payment of damages to other participants in the event that they are penalized by Roskomnadzor for non-payment of the duty.

-

Configuring the company’s internal processes related to actions required on its account on the Roskomnadzor website for the payment of the advertising duty, including timely response to various notifications from Roskomnadzor.

-

Analysing related tax issues that may arise in connection with the need to pay the advertising duty and adapt the company’s approach to doing business, such as the deduction of expenses for the payment of the advertising duty and advertising expenses for profit tax purposes.

The B1 team is ready to provide professional support on all the aspects listed above.

AUTHORS

.jpg)

Natalia Khobrakova

B1 Partner

Tax, Law and Business Support

Contact

.jpg)

Vadim Ilyin

B1 Partner

Tax, Law and Business Support

Contact

.jpg)

Vasilisa Asanova

B1 Senior Manager

Tax, Law and Business Support

Contact

.jpg)

Kristina Naumenko

B1 Assistant Manager

Tax, Law and Business Support

Contact

OTHER PUBLICATIONS

View all

Transfer pricing in UAE: declaration period and new FTA explanations

With the 30 September 2026 deadline for filing the 2025 corporate tax return approaching, companies should focus on ensuring the accurate disclosure of transactions with Related Parties and Connected Persons in the TP Disclosure Form.

10.06.2026

UMMC: revised time limits for decisions to initiate transfer pricing audits

On 29 April 2026, the Moscow District Arbitration Court issued a ruling in the Ural Mining and Metallurgical Company case No. А40-72524/2025 regarding the time limits for ordering transfer pricing audits of tax calculations and payments in related party transactions. Both at first instance and on appeal, the case was ruled in favor of the taxpayer, but these rulings were quashed by the court of cassation.

08.05.2026

.jpg)

Currency regulation in Kazakhstan: transactions lacking apparent economic substance

In April 2026, amendments to the Rules for Currency Transactions in the Republic of Kazakhstan entered into force, introducing, inter alia, the concept of transactions lacking apparent economic substance.

05.05.2026

Draft procedure for payment of technology fee published

The Russian Ministry of Industry and Trade has published a draft Government Decree establishing the procedure and deadlines for the payment of a technology fee. The Fee is scheduled to come into force on 1 September 2026 and, as previously reported, it will apply to electronic devices that are manufactured in or imported into Russia. The Fee will be payable by manufacturers and importers of such devices – both legal entities and individual entrepreneurs.

23.03.2026

.png)

Regulatory and tax control shifts in the IT sector: areas to focus on in early 2026

The end of 2025 was marked by numerous changes in IT regulation. When considered as a systemic whole rather than individually, they indicate several trends that should be taken into account when assessing tax risks and opportunities for software and database developers – including members of corporate groups – and their clients.

16.01.2026

.jpg)

Uzbekistan tax alert – 2026 legislative changes

In November 2025, the Ministry of Economy and Finance of the Republic of Uzbekistan released a draft budget message outlining several proposed tax policy changes effective from 2026. The implementation of the proposed measures is contingent upon the adoption of the corresponding amendments to the tax code of the Republic of Uzbekistan in December 2025.

16.12.2025

.jpg)

Bill amending the Tax Code passes the second reading in the State Duma

On 18 November, the Russian State Duma adopted in the second reading Federal Bill No. 1026190-8 “On Amendments to Parts One and Two of the Tax Code of the Russian Federation and Certain Legislative Acts of the Russian Federation”, which includes amendments proposed by the Government for the second reading of the Bill in the State Duma. After its third reading on 20 November, the Bill will be submitted to the Federation Council and then to the Russian President.

19.11.2025