Tax Messenger

Appealing against customs authorities' decisions via the administrative procedure

05.03.2024

The customs authorities are currently carrying out a large number of audits of foreign trade companies, both pre- and post-clearance, aimed at identifying violations of customs law.

As we have noted on a number of occasions in previous articles, one of the main matters checked in audits is whether or not the customs value of goods has been correctly stated where amounts of royalties and dividends have not been included in that value.

In view of the current tendencies in administrative practice and case law, decisions made on the basis of audits are subsequently contested by foreign trade companies using the following methods provided for in legislation:

- via the administrative procedure

- and (or) via the judicial procedure (see below).

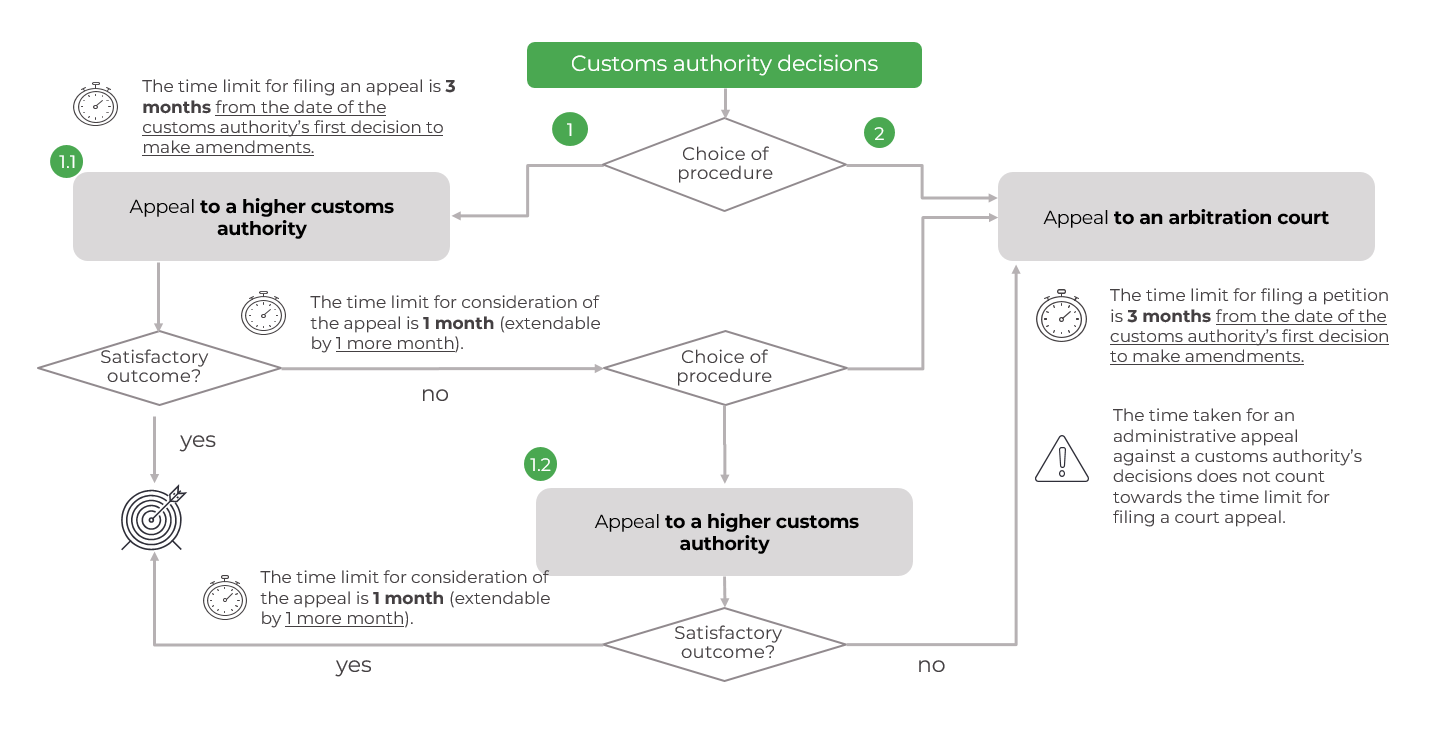

Appeal flow chart

Foreign trade companies still regard the administrative appeal method as ineffective compared with a judicial appeal owing to continued mistrust of the process of lodging an appeal within the same government department. The general view is that the receipt of a valid and reasoned appeal decision which overturns the decision of the lower customs authority is the exception rather than the rule.

Shift in emphasis from judicial to administrative appeal

With a view to reducing the level of conflict between the customs authorities and foreign trade companies, including as regards mistrust of the administrative appeal framework, the customs authorities are now attempting to foster an effective system of pre-court settlement of customs disputes.

In this context, the shift in emphasis from judicial to pre-court proceedings for the settlement of customs-related disputes is one of the key goals to be achieved by the customs authorities by 2030[1].

To achieve that goal the customs authorities are carrying out a whole range of measures, from making companies aware (through official websites, email, oral consultations, etc.) of the administrative appeal procedure and its advantages to making efforts to observe the principle of the full and thorough (objective) consideration of appeals.

What do the statistics say?

In 2023, on average, the customs authorities upheld 53% of appeals against decisions. The figure is higher for some regional customs administrations: for example, the Central Customs Administration upheld 58%.

To evaluate the administrative appeal process, it is essential to study the potential risks of using it as well as to identify its advantages over the judicial route.

Risks associated with administrative appeals and possible ways of overcoming them

Repeat performance of customs control measures

Decisions to uphold appeals often result in the repeat performance of customs control measures to rectify irregularities that occurred in previous inspections, followed by the adoption of new decisions and the repeat assessment of outstanding customs charges.

However, most post-clearance audits take place at the tail end of the three-year customs control period (for example, regarding those concerning the inclusion of amounts of dividends in customs value), and in those circumstances the customs office would have no grounds to carry out additional inspection measures.

Position of the higher authorities

Quite often, the position taken by the customs authorities derives from instructions and guidance issued by higher authorities such as the Federal Customs Service and the Ministry of Finance. In this case, attempts to challenge decisions on their merits will not, in the vast majority of cases, yield the desired outcome.

However, it is possible to argue that decisions are unlawful by pointing to procedural and methodological irregularities that occurred in the course of customs control, and this may be sufficient for decisions to be overturned.

The customs authorities' system of performance ratios

The Federal Customs Service has set lower customs authorities a target ratio for the “proportion of customs authorities’ decisions annulled through judicial and pre-court proceedings relative to the total quantity of declarations and customs authorities’ decisions adopted after the clearance of goods”. This ratio is calculated quarterly and should not exceed 0.23.

If the target is not met, the customs authorities must explain why. The ratio has a bearing on the overall performance appraisal of a customs authority and may result in its performance being deemed unsatisfactory.

If there has been a large number of annulled decisions in a given quarter, resulting in a high ratio, customs officials may be more inclined to reject an appeal.

Advantages

Despite the potential risks discussed above, besides the high success ratio for appeals by foreign trade companies the administrative appeal procedure has a number of substantial advantages:

-

No expenses in the form of state duty

-

Less time-intensive

-

Simplicity of the procedure

-

Rapid result

-

Availability of the judicial appeal route in the event of an unfavourable outcome – there is no risk of missing the deadline for filing a court appeal in this case

-

Full confidentiality

Filing an appeal electronically through a company's online account affords the following additional advantages:

-

No expenses for postal and courier services

-

No dependence on the working hours of post offices and customs authorities

-

Ability to track the status of the appeal review online

-

Ability to download documents from the declarant’s archives

In addition, foreign trade companies may avail themselves of the option of a face-to-face meeting with senior officials of the customs authority to put across their arguments in person.

Conclusions

Bearing in mind the appeal success rates, the advantages of the pre-court appeal procedure and the efforts being made by the customs authorities to steer companies towards this route and shift the emphasis away from judicial proceedings, we advise companies not to ignore the administrative appeal mechanism and to make full use of it in seeking redress for violations of their rights and legitimate interests.

If the judicial option is chosen straight away, it is unfortunately impossible, after going through all the court instances, to revert to the administrative procedure, whereas choosing the administrative route leaves open the option of attempting to settle the dispute in court at a later stage.

How can we help?

We have extensive experience of supporting appeals against customs authorities’ decisions through the administrative procedure. We know how to present the arguments of foreign trade companies to the officials who make decisions on appeals and have a track record of successful pre-court appeal outcomes.

Authors

- Wilhelmina Shavshina, Partner, Global Trade and Customs Services

- Ekaterina Sevostianova, Manager, Global Trade and Customs Services

- Radzhab Khanov, Senior, Global Trade and Customs Services

Show references

-

[1] Development Strategy for the Customs Service of the Russian Federation to 2030, approved by Directive No. 1388-r of the Government of the Russian Federation of 23.05.2020

OTHER PUBLICATIONS

View all

Transfer pricing in UAE: declaration period and new FTA explanations

With the 30 September 2026 deadline for filing the 2025 corporate tax return approaching, companies should focus on ensuring the accurate disclosure of transactions with Related Parties and Connected Persons in the TP Disclosure Form.

10.06.2026

UMMC: revised time limits for decisions to initiate transfer pricing audits

On 29 April 2026, the Moscow District Arbitration Court issued a ruling in the Ural Mining and Metallurgical Company case No. А40-72524/2025 regarding the time limits for ordering transfer pricing audits of tax calculations and payments in related party transactions. Both at first instance and on appeal, the case was ruled in favor of the taxpayer, but these rulings were quashed by the court of cassation.

08.05.2026

.jpg)

Currency regulation in Kazakhstan: transactions lacking apparent economic substance

In April 2026, amendments to the Rules for Currency Transactions in the Republic of Kazakhstan entered into force, introducing, inter alia, the concept of transactions lacking apparent economic substance.

05.05.2026

Draft procedure for payment of technology fee published

The Russian Ministry of Industry and Trade has published a draft Government Decree establishing the procedure and deadlines for the payment of a technology fee. The Fee is scheduled to come into force on 1 September 2026 and, as previously reported, it will apply to electronic devices that are manufactured in or imported into Russia. The Fee will be payable by manufacturers and importers of such devices – both legal entities and individual entrepreneurs.

23.03.2026

.png)

Regulatory and tax control shifts in the IT sector: areas to focus on in early 2026

The end of 2025 was marked by numerous changes in IT regulation. When considered as a systemic whole rather than individually, they indicate several trends that should be taken into account when assessing tax risks and opportunities for software and database developers – including members of corporate groups – and their clients.

16.01.2026